Daily Consumer #22 - Ecommerce Growth is Slowing. Long Live Ecommerce.

Daily Consumer #22 - Ecommerce Growth is Slowing. Long Live Ecommerce.

Plus GM launches its own used car marketplace.

My Work

Ecommerce Growth is Slowing. Long Live Ecommerce.

In Oct 2021, Romain Lapeyre, the CEO of Gorgias, commented that ecommerce’s period of strong growth is over. Data from the US Department of Commerce suggests that, as a percentage of total retail sales, ecommerce is now in decline. In short, stores are re-opening and a lot of demand is shifting back offline.

With the pandemic benefit behind us, what are the lessons for merchants? Should investing in ecommerce capabilities continue to be a focus? A few thoughts.

Ecommerce growth is harder to achieve for SMBs. For small online merchants, 2021 was a year defined not by the pandemic, but by privacy changes that dramatically impacted how brands could acquire customers online. Performance marketing channels like Facebook, long the primary growth mechanism for small brands to get in front of their desired audiences due to deep targeting capabilities, became much less efficient. To counter this, brands tried to shift to new strategies like influencer but largely could not achieve the same level of efficiency and scale. My expectation is that smaller brands will continue to struggle for the near future until new distribution opportunities emerge. I think this will happen though and early examples are emerging:

Co-op Commerce is enabling brands to drive traffic to one another.

Shopify may be enabling a new discovery layer itself via Shop app.

Lustre is building a new ecommerce-focused search engine.

Roku and Fire TV are reaching scale in connected TV, allowing brands to get in front of consumers on the bigger screen.

Roblox and Rec Room may allow brands be to discovered in the metaverse.

And if ecommerce growth isn’t possible to achieve, companies like Faire and Ankorstore may help small brands shift their businesses offline via their digital marketplaces that connect brands to retailers.

Enterprise-scale brands and retailers are all-in on ecommerce. While SMBs may be struggling to grow their ecommerce businesses, enterprise-scale brands and retailers are not. Large brands tend to have better margins due to economies of scale, have larger marketing budgets especially for driving brand awareness, and can build brand recognition offline which benefits them online. The big focus for these brands and retailers is to now close the loop between their offline and online businesses, which brands like Nike are doing by shuttering wholesale relationships which they don’t get customer data through. Some proof points on how large brands are growing:

Estee Lauder now sees 40% of its US beauty sales coming from online channels, up 2x from 2019.

Nike saw ecommerce sales grow 25% YoY in their fiscal Q1 2022, which now represents 21% of total sales. US ecommerce sales grew 40% YoY.

Levi’s saw ecommerce sales grow 75% YoY in their fiscal Q2 2021, which now represents 23% of total sales. This is up from 10% in 2015.

Procter & Gamble saw ecommerce sales grow 35% YoY in their full year fiscal 2021, which now represents 14% of total sales.

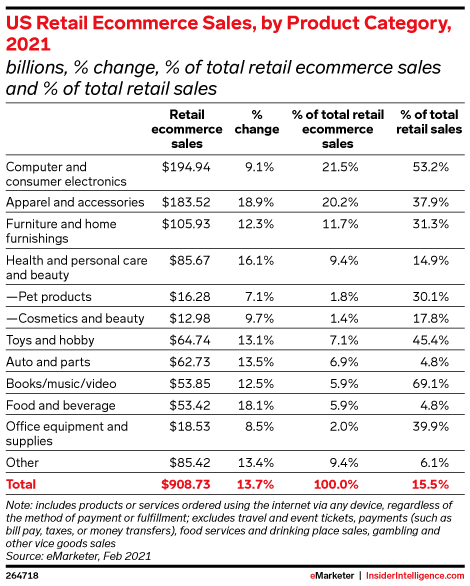

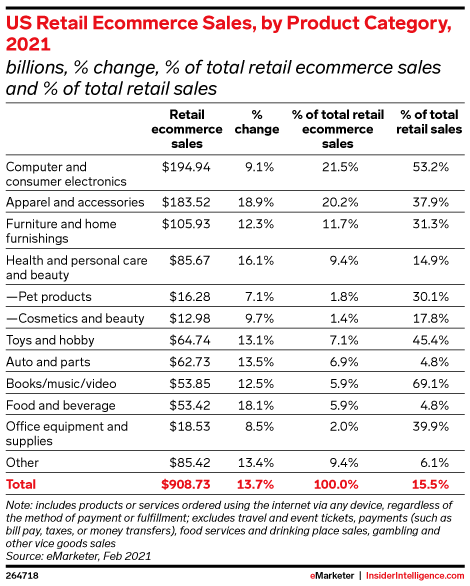

Certain product categories are still seeing strong ecommerce growth despite the headwind of store re-openings. While growth is slowing for ecommerce as a whole, certain categories continue to see elevated growth. Those categories specifically are fashion, food, and health and personal care. Fashion is bouncing back as people re-enter the world and want to look their best. Food is benefitting from the increased convenience of delivery, supply chain challenges for grocers, and the increasing fragmentation of taste. Health and personal care spend is similarly shifting online due to wider selection of products, especially around emerging trends like clean beauty and products that are more personalized for the consumer.

Ultimately, the core asset for a merchant is customer data, not stores, websites, or inventory. In my opinion, it’s incorrect to think about commerce through the lens of channel or product category. Ultimately, commerce is about understanding who your customer is, learning about what they need at any given time or inspiring them to “want” something, and communicating with them to match a product with that need or want as seamlessly and delightfully as possible. Stores are particularly good mechanisms to inspire “wants”. Ecommerce is a particularly good mechanism to solve “needs”. Both are important. And having unified data that gives you a singular view into who your customer is and how they behave is the most important thing of all.

Community

My firm is hosting our annual Index Ventures AI Summit on Jan 19-20th. Register for free here.

Shopify releases their 2022 Future of Ecommerce Trend Report. Highlights supply chain challenges, increased competition for pure-play ecommerce brands, the rise of social commerce, and the return of in-store shopping.

Okendo is hosting a panel on Top Trends for DTC Beauty Brands in 2022 on Jan 25th. Register for free here.

Shipbob is hosting their Ecommerce Unpacked Summit on Jan 27th. Register for free here.

News

Beauty.

A great breakdown of what it takes to make a personal care company successful.

Shiny hair, which suggests healthy hair, is the next big trend in beauty.

A profile on how Olaplex went from being a salon-focused haircare brand to being a dominant DTC brand. “Wong credits the brand’s growth in part due to a trend she calls ‘skin-ification of hair.’ Consumers’ approach to hair care is increasingly resembling their approach to skin care.”

Products focused on sensitive skin are all the rage. “At P&G, surveys found that “more than 65% of consumers say that they have experienced signs of sensitivity like redness, dryness, dry patches or a stinging/burning/itching sensation on their facial skin, and 83% are actively looking for skin care products that are created ‘for sensitive skin’ or that are ‘fragrance-free.’”

BNPL.

Cotopaxi partners with Sezzle to enable BNPL for its customers. Sezzle now has 44K online and in-store merchant partners.

APEXX Global enters the US BNPL space after working with 120 partners in European markets.

Ecommerce Search.

Walgreens starts using Algolia to power search on its website and mobile apps to help shoppers find relevant items available locally.

Food and Beverage.

Corona launches Corona Sunbrew, a non-alcoholic beer that contains 30% of daily value of vitamin D.

Grocery.

Instacart is expanding into ready-made meals which can be delivered in <30 minutes in 35 states. Grocery stores are becoming restaurants.

Holiday Shopping.

According to Adobe, US consumers spent $204.5B between Nov 1st and Dec 31st, which was up 8.6% YoY. Mobile accounted for 43% of total sales and had a conversion rate of 2-3%. Desktop had a conversion rate of 4-6%.

According to Salesforce, holidays sales between Nov and Dec grew 9% YoY to $257B. Luxury handbags (+45%), home furniture (+34%), and general footwear (+32%) were the fastest growing categories YoY. BNPL accounted for 8% of all online purchases, up from 6% the year prior. Apply Pay grew 68% YoY to 4% of all online purchases.

According to Klaviyo, total orders were up 10% YoY between Nov 26th and Dec 25th. AOV was up 18% YoY.

Home Goods.

Large retailers like Target, Container Store, Walmart, Amazon, and others are investing in home organization offerings as a product category. “We’ve seen a significant increase in demand for home storage and organization.”

Influencer-Driven Commerce.

Tom Brady officially launches his fashion brand, BRADY. Is working on it with some of the folks who built Skims, Kim Kardashian’s bodywear brand. “I’ve always felt like if I wear something, I want it to be something that’s gonna look good 25/30 years from now when I look back on old pictures. So creating something that was really timeless and creating things for all these different aspects of life that match these multifunctional lives that we have nowadays.”

Kanye West, Balenciaga, and Gap are setting up a 3-way collaboration called Yeezy Gap with items “ engineered by Balenciaga.”

Lululemon partners with Leylah Fernandez, a 19-year-old tennis star who us ranked #24 in the world, in a formal push into the tennis market.

Shaun White is retiring from snowboarding soon and will launch his own product brand called Whitespace, which will offer gear for snowboarding, hiking and hanging out at home.

Conor McGregor releases his brand of connected MMA gloves called FAST.

Inventory Management.

Retailers often don’t know where >10% of their inventory is located at any given time. RFID tags may be the solution. “Lululemon now tags all of its inventory, giving it a bird’s eye view that allowed it to ship online orders from stores even when they were closed during the early days of the pandemic because it could access product at any point across our network.”

Carter's and Under Armour are rolling out RFID, in partnership with Nedap iD Cloud, across their stores and warehouses to improve inventory accuracy.

Live Shopping / Social Commerce.

Whatnot, a live shopping app for collectibles, is partnering with UFC star Jorge Masvidal. Jorge will operate his own channel on the app, called The BRKRZ, on a weekly basis and will auction off sports cards, merchandise, and his fighting equipment.

Accenture releases their “Why Shopping is Set for a Social Revolution” report which estimates that social commerce will drive $1.2B of commerce by 2025.

TikTok is targeting $12B in ad revenue in 2022, up from $4B in 2021.

Amazon is struggling to get their live shipping product off of the ground. “Only had 30-70K active viewers during Prime Day 2021.”

Kylie Jenner becomes the first woman to reach 300M followers on Instagram.

Instagram reclaimed the #1 spot from TikTok in terms of worldwide app downloads in Q4 2021.

Logistics / Supply Chain.

Seth Winterroth shares his thesis on why collaborative robots will become widely adopted in the supply chain.

An excellent video by CNBC unpacking Amazon’s strategy of vertically integrating its supply chain to get around gridlock in ports, etc.

Hugo Boss is moving its a large portion of its manufacturing to Turkey from SE Asia to increase the reliability of getting products on time and to customers more rapidly.

Robotic arms are increasingly making their way into warehouse operations.

USPS delivered more than 13.2B letters and packages during the 2021 holiday season.

Luxury.

LVMH deepens its relationship with Chinese marketplace JD.com. LVMH brands that have greenlit partnerships with the platform include Louis Vuitton, Berluti, Givenchy Beauty, Benefit Cosmetics, Bulgari, Guerlain, Dior, Loewe, and most recently, Givenchy. “Luxury sales on the platform have seen annual growth of over 200% YoY since 2019.”

Macroeconomics.

Marketplaces.

Shopee hosted their 2022 Shopee Brands Summit and announced several updates including new features like Shopee Live and a new mega shopping event on March 15th.

LionTree shares a great overview of marketplace business models and what makes them powerful. Features marketplaces like Faire, StockX, Back Market, OpenSea, and more.

Metaverse.

Adweek argues that brands shouldn’t ignore the metaverse as 1) consumers crave experiences, 2) the entire customer journey can happen within the metaverse, 3) it takes co-creation to the next level, and 4) it powers inclusivity, diversity and representation.

Gap announced the launch of its first NFT collection in collaboration with Brandon Sines, the maker of Frank Ape. “The gamified experience encourages customers to collect iconic Gap hoodie digital art at the Common and Rare levels to unlock the opportunity to purchase the Epic, which is limited edition digital art by Brandon Sines and a physical Gap x Frank Ape by Sines hoodie.”

Balmain and Barbie recently collaborated on a collection of 3 NFTs and physical products. “Connecting to culture is a core component of Mattel’s Playbook, and Barbie is a globally recognized icon in fashion and pop culture, which creates an interesting intersection between the brand, art and collectability.”

Investors are speculating on virtual plots of real estate in Decentraland, a virtual world powered by the Ethereum blockchain. “If you think about cities in general, in New York you have Fifth Avenue and in LA you have Rodeo Drive. We want to create the equivalent of those streets in the metaverse.”

Shaq is planning to release “non-downloadable virtual footwear, clothing, headwear, and eyewear for use in virtual environments.”

Omni-Channel Commerce.

Savage X Fenty, Rihanna’s lingerie brand, is opening 5 stores in the US in 2022.

Billie, a DTC women’s razor brand, is launching its products in Walmart locations nationwide.

Babylist launches ‘Cribs’, a pop-up experience hosted in a LA home to help visualize great environments for babies.

Payments.

A good Twitter thread on why Shop Pay may have been the big winner of the holiday season.

Fast announces a partnership with Marquee Brands to bring one-click checkout to their brands including Martha Stewart, BCBGMAXAZRIA, Ben Sherman, Body Glove, and Motherhood Maternity.

Wix partners with Nuvei for payment processing for its merchants.

Resale.

Timberland is launching Timberloop, a refurbishing program for used products. Customers who send in their used products receive a 10% discount on their next purchase. Refurbished products will be resold on a soon-to-be launched secondhand portion of Timberland’s main website.

Bring a Trailer, an online auction-based marketplace for vintage cars, sells $829M of vehicles in 2021, up 108% YoY.

GM is launching CarBravo, its own used-vehicle platform. “CarBravo gets first pick of the 400K vehicles in pre-owned inventory from Chevrolet, Buick and GMC dealers, plus vehicles that GM Financial re-possesses.”

Same-Day Delivery.

Girl Scout Cookies partners with Doordash to sell its cookie products on Doordash’s marketplace.

CloudKitchens is expanding into retail. The company is acquiring liquor stores and turning them into fulfillment centers to form the basis for a delivery service that delivers alcohol and packaged goods in under 30 minutes, starting in LA.

Sustainability.

Proposed legislation called the Fashion Act is being discussed among certain states which would “require global apparel and footwear companies operating in New York to set binding targets to reduce their environmental impacts based on mandatory reports. Brands that don’t comply may have to pay as much as 2% of revenues over $450M as a penalty.”

TV Marketing.

NBC is investing in an ad platform that will allow advertisers to reach NBC’s network of 50M households and 150M individuals. TV ads in the future may become very personalized.

Google supposedly now has 110M monthly active connected TV devices across Google TV and Android TV.

Disney, Netflix, and the 6 other top content studios will spend $115B on content production in 2022.

Funding and Exits

Brands

Alcohol.

Monster Beverage Corp acquires CANarchy Craft Brewery Collective, a maker of craft beer and hard seltzer, for $330M. “The deal is a springboard for Monster into the alcoholic beverage space.”

Apparel.

We11done, a DTC South Korea-based fashion brand known for its “youthful approach to unisex design”, sells a majority stake to Sequoia Capital China and plans to expand its presence in China.

The House of LR&C, a fashion brand started by Russell Wilson and Ciara, is raising $20-50M.

Beauty.

Oddity, the parent company of Il Makiage, raises $130M from Thomas Tull, Franklin Templeton, and others at a $1.5B valuation for its tech-driven beauty brand that includes a foundation-matching system. “Il Makiage reported $260M revenue in 2021 and is profitable.”

Brand Rollups.

Thrasio acquires Lifelong Online, a brand portfolio spanning kitchen, home, lifestyle and healthcare. Also plans to set aside $500M to acquire brands focused on India.

Ecommerce Brands raises $40M in debt and equity from Bearing Ventures to acquire DTC brands, integrate them on Cart.com and grow them in revenue and profitability.

Eyewear.

Mojo Vision raises $45M from Amazon Alexa Fund, PTC, Edge Investments, and others for its AR contact lenses that aim to overlay sports and fitness data without obscuring vision. Has initial partnerships include Adidas Running (running/training), Trailforks (cycling, hiking/outdoors), Wearable X (yoga), Slopes (snow sports), and 18Birdies (golf).

Fabric.

MycoWorks raises $125M from Prime Movers Lab for it mushroom-based leather alternative fabric used by fashion brands for sustainable clothing. Will invest in a larger production facility.

Food and Beverage.

Gousto raises $100M from Softbank at a $1.7B valuation for its UK-based meal kit delivery service that offers over 60 recipe kits.

Footwear.

Tecovas raises $56M from Elephant for its western footwear and apparel brand.

Medical Wear.

Jaanuu raises $75M from Eurazeo for its DTC brand of medical scrubs. Competes with Figs.

Personal Care.

Harry’s raises $140M from a syndicate of investors including Zola’s co-founder Shan-Lyn Ma, Addition founder Lee Fixel, Campbell Soup CEO Mark Clouse, Zoom chief diversity officer Damien Hooper-Campbell, and others for its shaving products-focused brand.

Petcare.

Fable raises $9M from 14W for its pet accessories brand which features collars, leashes, and toys.

Streetwear.

Heat raises $5M from Antler and LVMH for its streetwear-focused mystery box service that aims to give consumers more value than what they pay for.

Marketplaces

B2B Commerce.

Ankorstore raises $283M from Bond and Tiger Global at a $2B valuation for its Europe-focused marketplace connecting 15K brands with 200K retailers in 23 countries.

Inxeption raises $275M in debt and equity from Schonfeld Strategic Advisors at a $3B valuation for its B2B marketplace for industrial equipment. “Revenues grew over 400% YoY, we crossed over $100M in annualized revenues, and we have a rapidly growing customer base of over 1K customers.”

Tul raises $181M from 8VC at a $700M valuation for its marketplace connecting construction material suppliers with SMB retailers in Latin America. “Expects to reach 10K customers in Brazil by the end of 2022.”

NFTs.

Flip raises $6.5M from Distributed Global and Chapter One for its app that aggregates and allows users to search for NFTs across marketplaces in one place, making discovery easier.

Omni-channel Retail.

Foxtrot raises $100M from D1 Capital Partners for its omni-channel convenience store business. 30% of their business is private label. Revenue doubled in 2021. Plans to open 25 new stores in 2022.

Petcare.

Laika raises $48M from Softbank for its Latam-focused marketplace for pet products. “Serves more than 300K active users who get products delivered within 2 hours.”

Resale.

StockX, a resale marketplace for sneakers and other high-value goods, plans to go public in H1 2022.

Back Market raises $510M from Sprints Capital at a $5.7B valuation for its marketplace for refurbished electronics. “6M customers have purchased a device on Back Market. Our goal is to make refurbished electronics the first choice for tech purchases.”

Twig raises $35M from Fasanara Capital for its resale marketplace that gives sellers instant offers on fashion and electronics but first requires users to sign up for a Twig debit card. Claims to have 250K users in the UK.

Same-Day Delivery.

Bolt raises $709M from Sequoia Capital and Fidelity at a $8.4B valuation for its Europe and Africa-focused super app that offers on-demand ride hailing, shared cars and scooters, and restaurant and grocery delivery. “Is now in over 400 cities and reaches 100M customers across Europe and Africa.”

Arive raises $20M from Balderton Capital for its same-day delivery service that delivers non-grocery goods rapidly. The Arive app has already been downloaded >100k times.

Software

Analytics.

Daasity raises $15M from VMG Catalyst for its analytics platform serving ecommerce merchants. Enables brands to pull in all of their data from different places, like Shopify, Amazon, Facebook and Klaviyo, analyze it, and act on it. “Has 1.6K customers including Manscaped, Vuori and Caraway Home, and in the past year grew its annual recurring revenue by 300%.”

Headless Commerce.

Swell raises $20M from VMG Catalyst and Headline for its suite of ecommerce APIs to enable customized ecommerce storefronts. “In the past year, Swell grew revenue 5x and grew its customer base to over 1K customers after starting the year with 30 customers.”

Restaurants.

Flipdish raises $100M from Tencent and Tiger Global at a $1.25B valuation for its online ordering system that powers restaurants in 25 countries. “More restaurants started launching first-party ordering channels rather than relying on aggregators like DoorDash and Uber Eats. Customers range from independents to chains and ghost kitchens.”

Parrot raises $9.5M from F Prime Capital for its Mexico-focused software for restaurants that centralizes and streamlines operations for delivery orders. Has 500 customers currently.

Fintech

Checkout.

Bolt raises $355M from BlackRock at an $11B valuation for its one-click checkout platform. “Over the past year, Bolt grew its GMV per merchant by 80% while transactions grew 200% YoY. The company also says 100M shoppers are poised to join the Bolt network over the next 18 months.”

Payment Orchestration.

Gr4vy raises $15M from March Capital for its cloud-native payments orchestration platform that acts as a conduit between merchants' shopping carts and payment providers. “Worldwide growth in various payment methods and processors has led merchants to build increasingly complex payment infrastructure that's highly inflexible when it comes to the fintech and payments market.”

Payment Processing.

Checkout.com raises $1B from Franklin Templeton and QIA at a $40B valuation for its digital payment processing service. Plans to expand more aggressively into the US and cater increasingly to crypto companies. “The company’s payment volume tripled in both 2020 and 2021.”

Refund Insurance.

Seel raises $17M from Lightspeed for its return assurance service which puts the cost of refunds and returns on Seel instead of the merchant in exchange for an upfront fee. Is being used by 200 merchants. “Is seeing 20% of shoppers adding the assurance to their orders, which translates to a 5% conversion lift for merchants.”

Save Now, Pay Later.

Accrue Savings raises $25M from Tiger Global for its save now, pay later product. Allows merchants to help their shoppers save up to purchase one of their products. Accrue opens a savings account on behalf of the shopper. Currently has 15 customers including Allbirds, Casper, Poly & Bark, Smile Direct Club and Tire Agent.

Logistics

Ecommerce Fulfillment.

Ryder acquires Whiplash, an ecommerce fulfillment service provider, for $480M. Whiplash serves 250 brands across 19 warehouses. Ryder also acquires Midwest Warehouse & Distribution System.

Cart.com acquires FB Flurry, an ecommerce fulfillment service provider for DTC brands. Distributes more than 35M units from 4 warehouses.

Shipment Tracking Software.

Project44 raises $240M from TPG, Thoma Bravo, and Goldman Sachs at a $2.4B valuation for its software platform that serves as “connective tissue” for shippers, logistics providers and other stakeholders in the transportation industry and tracks >1B packages annually and 96% of all shipping containers in the world. “Reached $100M in in annual recurring revenue and is targeting about $170M by year-end 2022.”

Product of the Week

Tom Brady just launched his fashion brand, BRADY, so I figured I’d make it the product of the week. I’m personally not a big believer in celebrity-driven brands, especially ones where the brand is named after the celebrity. Celebrities have fairly short “shelf lives” of 10-20 years for the most part, so it’s hard for me to believe that their brands will be any more enduring. Plus, they are running multiple businesses at any given time (in this case, being an athlete), so it’s hard to believe that the celebrity can channel the energy needed to make a product brand successful. Skims is a counter-example. Curious if you have thoughts on this broader trend. You can buy BRADY apparel here.